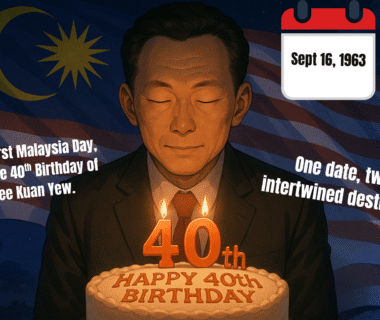

Happy Malaysia Day to all of you who are from Malaysia!

On another and related note, those of you who know me probably know that I am a big fan of Lee Kuan Yew.

Well, that’s a bit of a small understatement. I mean, it would have to be for someone who was somehow so moved that he decided to write an entire book about Lee Kuan Yew, which is by the way exactly what I did.

This Malaysia Day, 16 September, I’m very happy to announce the release of “One Date, Two Destinies: Lee Kuan Yew and the Birth of Malaysia and Singapore”, at a (Malaysia Day) discount!

This was a fun project to engage in, writing about the entire track of Lee Kuan Yew’s history from his birth up until the end.

I think it is crucial to look back at the past to understand history better, and this is one of the first things that a person will understand, I think, if they look just a little bit beneath the surface of Malaysian history and that which we call Malaysia.

I don’t think that there is quite a project that is like this, but I think that it was an extremely fun one – It contains many of my own personal reflections about Mr. Lee and the role that he played in Malaysia and Singapore, and in our shared history together, one that was born from a time of what can rightfully be called trauma.

I hope that you will find it meaningful and valuable for your own personal development and growth even as you reflect on these stories.

Thank you for your support in advance if you would like to purchase the book!

Two nights ago, the Prime Minister’s Office of Singapore posted an excellent talk by Singaporean Senior Minister Lee Hsien Loong at the 69th Economic Society of Singapore annual dinner!

There is plenty to learn about and a ton of different insights on many different topics from SM Lee, and I highly recommend anyone who is interested in the economics of our changing world order to watch it with interest and even to consider taking notes.

There is plenty to learn here, from marginal thinking to tariffs to the realities of taking back a policy – and it is all very much worthwhile.

The only part that triggered me a little bit was when a lady representing Singapore’s GIC asked a question about the skill sets that will be important for the workforce in the age of generative AI; I made a small contribution on the page as such, and you can also read it here, through the pictures.

Here was my response.

SM Lee,

Thank you for the insightful talk, which offered me a lot of insight into trade policy, the politics intertwined with economics, the Pandora’s box that is Liberation Day tariffs, and so many other things!

It was packed with insights and many thoughts that I found were interesting to think about – I certainly will choose not to lie flat and hope to make a difference in many good ways, whether from where I am in Malaysia at the moment or in any eventuality of time when I should move to Singapore, which I would be happy to if the correct opportunity were to come along.

If I were to make a small contribution, SM, the lady from the GIC was asking specifically about generative AI, which is not in general the same as artificial intelligence and machine learning models that seem more pertinent to the examples you provided. Generative AI is more ChatGPT than medical diagnosis, and is more related to creating text, images, and videos upon prompting and making use of computing systems in order to create things that humans might otherwise not have the inspiration or understanding to be able to do – which encompasses anything from writing emails from bullet points – and then summarizing emails into bullet points!!! – to doing homework and in turn to generating pictures and even movies.

Perhaps part of the skill of functioning well in a generative AI world is knowing and understanding what it means to be human and how to accentuate and articulate that humanness in the face even of multiple AI-generated sources of influence, whether to appeal to others who are also human through personality and advocacy or being able to distinguish what was artificially generated from what was humanly made to finer and finer degrees even as we become more integrated and AI in turn shapes our patterns of thought.

I would further add to that that at 43:56 you said “automatic” general intelligence, Sir.

If I may make a small correction, it is actually Artificial General Intelligence; although it is yet to come fully into existence, the challenges that it poses, I think, are not just about what statistical models can produce, but in turn also touch upon the question of whether it can self-improve and get to a point whereby it becomes independent of human beings – a notion that is very interesting, philosophically speaking, though it is unclear that in the scenario of existence of such a thing, the concept of moving to another industry would be relevant.

It is definitely logical to think about what the technology can do at this point and to understand its implications and possible uses and how it can translate into second- or third-order effects as the technology changes.

We are left fundamentally still with the problem of managing how human beings live, work, interact, and negotiate the boundaries of a world that is changing and has changed in both this era and beyond.

Thank you again for your sharing, and I look forward to learning more from you in the future – if at a later point you will take up my invitation to join me on my podcast, I look forward to meeting you in that context then!

V.

Sorry for the irregular updates of late – will try to get back on track in a bit; enjoy the video!

If you were like me, these were words that you confronted in the course of your economics classes as a younger student. And if you are anything like me, they would have infuriated you as you wondered to yourself what it would mean to perform that strange, almost unavoidable injunction time after time as understanding eluded you and comprehension of what you were meant to do evaded your every grasp.

In today’s blog post, I hope to explain the difference to you and also to ground your understanding of what it means to analyze and to evaluate to make your economics journey that much smoother, that much easier, and hopefully just a little more meaningful than you might have expected it to be.

Ready? Let’s go!

Let’s start by revisiting something small, but fundamental and important.

Economics is the study of choice under scarcity. As we discussed before, that scarcity can take the form of pretty much anything and everything that is finite in this universe.

Most often we think of it as money, but it can also be time, or anything else that we could use to serve a goal in our universe.

Okay, great. Now have a look at the analysis and evaluation assessment objectives for a quick bit.

All right, you’ve probably seen that before – it’s also relevant for IB Economics since all we really are interested in is just the general idea or concept of what this set of topics mean, so now let’s refresh everything a little bit.

Let’s first talk about analysis.

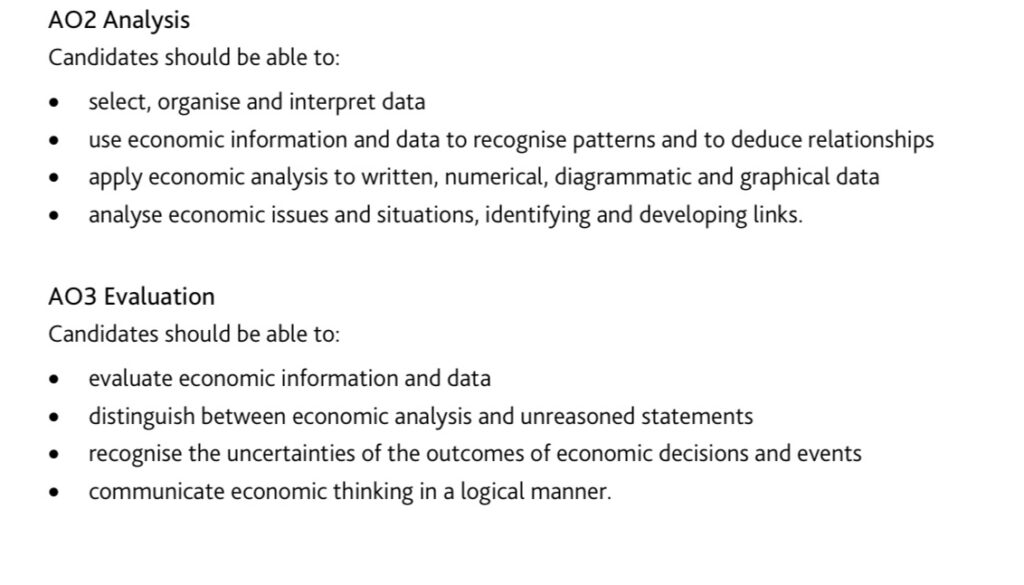

You’re told that analysis means that you’re able to select, organize, and interpret data. You should be able to use economic information and data to recognize patterns and to deduce relationships, and apply economic analysis to written, numerical, diagrammatic, and graphical data and analyze economic issues and situations, identifying and developing links.

Sounds like a mouthful?

Sure, but here’s another way you can think about it.

Think about it as understanding the results of a choice.

Analyzing in economics is understanding and knowing consistently how to answer this question: what will happen if we make this choice according to economic theory?

Here you can see why the diagrams come in because you need to be able to look at something that’s happening and understand how to apply the theory and what would happen according to the theory in the situation that you’re describing.

For example, if for some reason there is extremely good weather for the season or somehow all of the seeds that you use for a crop happen to spontaneously evolve and begin producing a much higher yield, what happens is that clearly more crops can be supplied at every single given price and you should be able to predict that a supply curve would then shift to the right based on that.

On the other hand, there is evaluation, which is a little bit trickier.

Same with the other assessment objective, we know what that looks like for the IGCSE and A levels as well.

Evaluation, in the context of IGCSE/A Level economics, means being able to evaluate economic information and data, distinguish between economic analysis and unreasoned statements, recognize the uncertainties of outcomes of economic decisions and events, and communicate economic thinking in a logical manner.

Think of evaluation as trying to decide if your choices make sense, the impacts of your choices on other people, how the choice could play out under different situations whether in the short-term or the long-term, and how your choice could affect different people or parties, amongst other things.

In both cases, you are thinking and reasoning about choices across time frames, considering how choices affect others, yourself, and thinking about how scarce resources are used, provided, and distributed throughout our society.

If this seems a little vague, it is often because you may not be thinking about the choices and the occurrences that may happen in our society and world from different points of view, or thinking deeply about how to understand the choices that we face in life.

That is natural because often times the world teaches us to take things as given. We are presented with a million different choices on a day-to-day basis and are so overwhelmed with them that it often becomes easy just to make choices all day. Well, that’s exactly the kind of thinking that economics trains you to participate in, and I think that it’s valuable to learn about it for that reason. Because it is relevant to everyone.

Now you might say that thinking about choice doesn’t necessarily mean that you should be learning about economics, and I totally respect that. But the framework that economics gives for thinking about choice I think is something that is definitely worthwhile to think about, so long as we live life on this planet and scarcity remains a real and lived out facet of human experience.